CoWoS Is the New Silicon Shortage: What Procurement Teams Must Know About the 2026 Packaging Crisis

Table of Contents

- The Rise of CoWoS

- Why is CoWoS Necessary?

- The 2026 Capacity Crunch

- How Packaging Bottlenecks Impact Global Procurement

- What Procurement Teams Must Do Now

- 1. Audit Your BOM for CoWoS Exposure

- 2. Qualify Alternative Packaging Sources Now

- 3. Build a CoWoS-Adjusted Lead Time Model

- 4. Protect Your Peripheral BOM

- 5. Engage TSMC’s OSAT Partners Directly

- Outlook: When Does Relief Arrive?

- References & Sources

⚡ Sourcing Summary

TSMC's CoWoS (Chip-on-Wafer-on-Substrate) advanced packaging is the primary bottleneck for AI logic chips in 2026. With 85%+ of 2026-2027 capacity pre-booked, 52-78 week lead times, and NVIDIA alone consuming ~60% of allocation, sourcing teams must actively monitor interposer capacity, qualify alternative packaging platforms (ASE FoCoS, Intel EMIB), and build buffer stock of peripheral BOM components exposed to the CoWoS ripple effect.

If you track the semiconductor supply chain in 2026, you will quickly notice a paradigm shift. For decades, Moore’s Law dictated that the primary chokepoint in chip manufacturing was shrinking the transistor on the silicon wafer. Today, the foundries can produce 3nm and 2nm logic dies with relatively high yields.

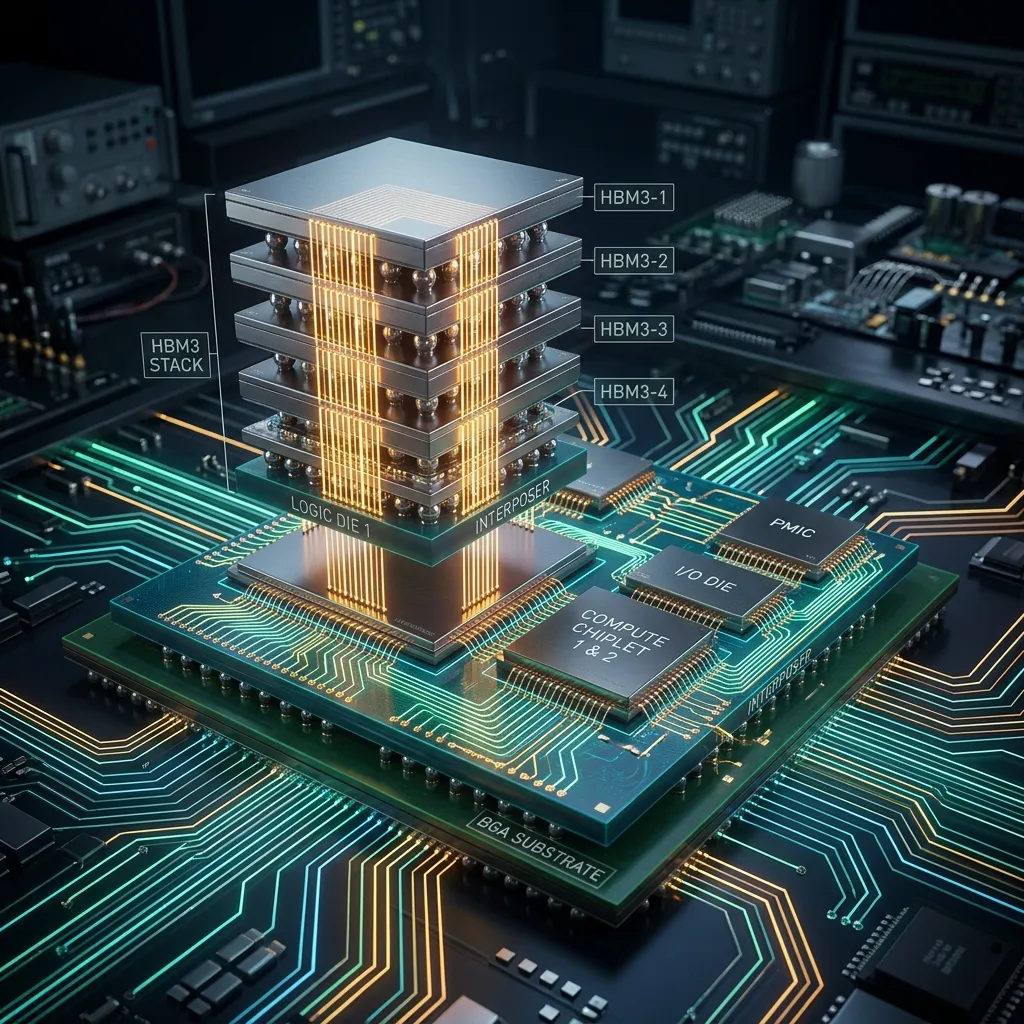

The true bottleneck preventing hyperscalers from deploying AI data centers at their desired speed is no longer the silicon fabrication itself—it is Advanced Packaging. Specifically, the 2.5D and 3D packaging technologies required to connect high-performance logic chips with High Bandwidth Memory (HBM).

The Rise of CoWoS

At the heart of the AI hardware boom is TSMC’s Chip-on-Wafer-on-Substrate (CoWoS) technology. High-end AI accelerators from Nvidia, AMD, and custom ASIC designers rely entirely on CoWoS or equivalent 2.5D packaging.

Why is CoWoS Necessary?

Traditional organic substrates cannot support the microscopic interconnect densities required to link a massive GPU logic die to surrounding HBM stacks. CoWoS solves this by placing the chips on a silicon interposer, which acts as a microscopic bridge, allowing terabytes of data to flow between logic and memory per second.

The 2026 Capacity Crunch

Despite aggressive capital expenditure and rapid facility expansion by TSMC, Amkor, and Intel Foundry Services, advanced packaging capacity remains heavily allocated throughout 2026. Here is the data procurement teams need to internalize:

| Metric | Value | Source/Period |

|---|---|---|

| TSMC CoWoS Capacity | ~120,000-140,000 wpm | Mid-2026 |

| OSAT Partner Capacity | ~50,000-60,000 wpm | Mid-2026 (ASE, SPIL, Powertech) |

| Total Advanced Packaging | ~170,000-200,000 wpm | Mid-2026 |

| Capacity Pre-Booked | 85%+ | 2026-2027 |

| NVIDIA Allocation Share | ~60% | 2026 |

| Lead Time (CoWoS-S / CoWoS-L) | 52-78 weeks | As of mid-2026 |

| Supply-Demand Gap | ~10% shortfall | Narrowed from ~20% in late 2025 |

The capacity ramp has been extraordinary by any historical standard — CoWoS output has roughly tripled since 2023 — but demand is compounding even faster. TrendForce projects AI accelerator wafer demand rising 11x between 2022 and 2026, and each new GPU generation consumes larger interposers with more HBM stacks, so per-chip packaging area keeps rising. The result: even an aggressive capacity ramp arrives short.

Setting up a new packaging facility requires specialized equipment—such as ultra-precise pick-and-place machines and advanced thermal compression bonders—which themselves suffer from 12-to-18-month lead times. The expansion cycle from committed investment to qualified production is approximately 36 months.

How Packaging Bottlenecks Impact Global Procurement

For procurement professionals dealing with electronic components, the CoWoS bottleneck creates a profound ripple effect across the entire BOM (Bill of Materials).

- The “Golden Screw” Problem: You cannot ship a $400,000 AI server rack without the primary accelerator. Consequently, OEMs are hoarding peripheral components (PMICs, voltage regulators, high-speed networking switches) while waiting for their GPU allocations. This artificial hoarding occasionally causes unexpected spot shortages in otherwise unconstrained commodity components.

- Chiplet Architectures Driving Complexity: To bypass reticle limits, manufacturers are heavily adopting “chiplet” designs. Instead of one massive monolithic die, they manufacture smaller dies and package them together. This drastically improves silicon yield but exponentially increases the demand for advanced packaging, exacerbating the capacity crunch.

What Procurement Teams Must Do Now

The advanced packaging bottleneck requires procurement teams to move from reactive sourcing to proactive supply chain engineering. Here are five concrete steps:

1. Audit Your BOM for CoWoS Exposure

Not every AI chip uses CoWoS — but if yours does, it is the single most fragile link in your supply chain. Request packaging type confirmation from your suppliers for every AI accelerator, GPU, and custom ASIC on your BOM. Key question to ask: “Does this part number require TSMC CoWoS, CoWoS-L, or equivalent 2.5D advanced packaging?” Chips using standard flip-chip BGA are not affected.

2. Qualify Alternative Packaging Sources Now

Even if you do not switch today, starting the qualification process for a second-source packaging platform buys you optionality. The three credible alternatives:

- Intel EMIB: Already shipping for AWS, Cisco, SpaceX. Google TPU v8e rumored for 2027. U.S.-based production.

- ASE FoCoS: Viable overflow for simpler chiplet designs. Shorter qualification cycle than EMIB.

- Samsung I-Cube: Gaining traction for non-NVIDIA AI accelerators.

Qualification takes 9-12 months per platform — start before you need it.

3. Build a CoWoS-Adjusted Lead Time Model

Standard lead time forecasts break down when the packaging step is oversubscribed. For CoWoS-dependent parts, budget:

- Minimum 52 weeks from order to delivery in mid-2026

- 78+ weeks if you are not a Tier-1 hyperscaler customer

- Add 4-6 weeks for peripheral component consolidation if you are building full systems

The CoWoS booking window is the leading indicator. Track it quarterly — when lead times start trending down across consecutive quarters, supply is genuinely loosening. Until then, capacity headlines about “expansion” do not translate into shorter wait times.

4. Protect Your Peripheral BOM

The Golden Screw effect means components you thought were unconstrained may suddenly go short. PMICs, voltage regulators, high-speed networking switches, and server-grade connectors are all vulnerable to artificial hoarding while OEMs wait for GPU allocations. Maintain 4-6 weeks of safety stock on critical peripherals for any system that includes a CoWoS-dependent accelerator.

5. Engage TSMC’s OSAT Partners Directly

TSMC is no longer the only game in town. ASE (FoCoS), SPIL, and Powertech collectively added 50,000-60,000 wpm of CoWoS-compatible advanced packaging capacity by mid-2026. For non-flagship AI chips, OSAT partners offer shorter lead times and more flexible allocation. Establish relationships with these suppliers now, even if your primary volume stays with TSMC.

📌 Next Steps: For the latest June 2026 capacity data and an analysis of TSMC’s next-generation CoPoS (Chip-on-Panel-on-Substrate) platform targeting the NVIDIA Feynman generation, see our follow-up: CoWoS to CoPoS: Is TSMC’s Next-Gen Advanced Packaging Finally Closing the Supply-Demand Gap?

Outlook: When Does Relief Arrive?

Our market intelligence indicates the CoWoS bottleneck will ease gradually rather than break suddenly. TSMC has successfully integrated new packaging plants in Taiwan (Tongluo, Chiayi) and Japan, and the supply-demand gap has narrowed from ~20% in late 2025 to ~10% in mid-2026. However, the insatiable demand from Generative AI and automotive ADAS continually absorbs new capacity as it comes online.

The critical milestone to watch: TSMC’s Arizona advanced packaging facility, expected to qualify in mid-to-late 2026 with volume production in 2027. This will be the first non-Taiwan CoWoS source, partially addressing the geopolitical concentration risk that has made advanced packaging a single-point-of-failure for the global AI supply chain.

For procurement teams, the playbook through 2027 is straightforward: treat CoWoS as a structurally constrained resource, not a temporary shortage. Diversify packaging sources, build lead time buffers, and protect your peripheral BOM. The teams that act now will be positioned to scale when capacity loosens; those that wait will find themselves at the back of a line that is already years long.

Navigating CoWoS-driven supply chain delays? SupplyICs leverages deep market intelligence and a global inventory network to help you source critical networking and logic components. Submit an RFQ or upload your BOM for a personalized quote within 24 hours.

References & Sources

- TrendForce — AI Server and Advanced Packaging Capacity Monitor (June 2026).

- TSMC — Advanced Packaging Technology Documentation and Q1 2026 Earnings Transcript.

- Silicon Analysts — CoWoS Lead Times: The Real AI Supply Bottleneck in 2026 (June 2026).

- JEDEC Solid State Technology Association — Standards for Semiconductor Packaging and MSL Traceability (J-STD-020 & J-STD-033).

- Semiconductor Industry Association (SIA) — 2026 State of the Global Semiconductor Supply Chain.

- Automotive Electronics Council (AEC) — AEC-Q100 Stress Test Qualification for Integrated Circuits.

Related SupplyICs Analysis:

- CoWoS to CoPoS: Is TSMC’s Next-Gen Advanced Packaging Finally Closing the Supply-Demand Gap? — June 2026 capacity update and CoPoS deep-dive

- Securing Mission-Critical FPGAs for AI Infrastructure: A 2026 Sourcing Guide — FPGA procurement strategy for AI systems

SupplyICs Sourcing Team

Contact Our TeamIndependent Component Specialists

A team of veteran buyers navigating the global spot market. We specialize in locating hard-to-find, shortage, and EOL components. From strict anti-counterfeit verification to cross-reference matching, we provide frontline data to help you secure authentic stock safely.